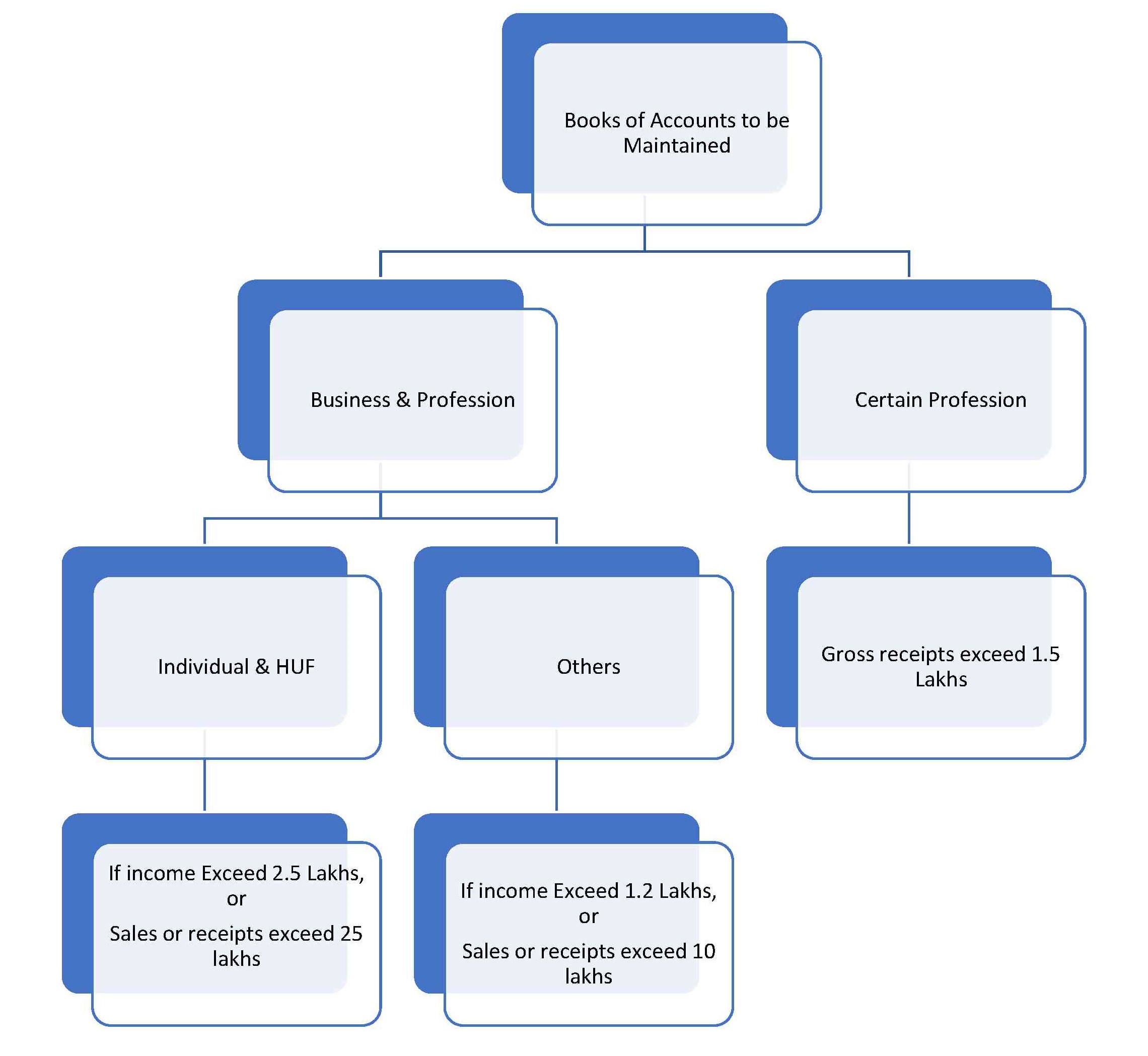

Books of Accounts to be kept by business and professional – Section 44 AA

Many of the businesses and professionals are always in ambiguity that which books & records to be kept as per Income Tax Act 1961. Today we will decode this complete Section 44AA of the Income Tax Act 1961. Section 44AA of the Income Tax Act 1961 is for Maintenance of accounts by certain persons carrying on profession or business.

Before going ahead, we must understand certain professional. Certain Profession here include person into :

1. Legal

2. Medical

3. Engineering

4. Architectural profession

5. Profession of accountancy

6. Technical consultancy

7. Interior decoration

8. Authorised representative

9. Film artist includes:

I. actor

II. cameraman

III. director, including an assistant director

IV. music director, including an assistant music director

V. art director, including an assistant art director

VI. dance director, including an assistant dance director

VII. editor

VIII. singer

IX. lyricist

X. story writer

XI. screen-play writer

XII. dialogue writer

XIII. dress designer

Certain professional not required to maintain any books

The total gross receipt in case of new setup in current year does not exceed one lakh fifty thousand and in old set up, the gross receipt should not exceed one lakh fifty thousand in any of the three previous years.

Need to maintain booked of accounts under Business & Profession:

A. For individual & HUF :

I. If the income exceeds Two lakh fifty thousand or total sales, turnover or gross receipt exceeds twenty five lakh rupees.

II. Newly set up business, income exceeds Two lakh fifty thousand or total sales, turnover or gross receipt exceeds twenty five lakh rupees.

B. For others :

I. If the income exceeds One lakh twenty thousand or total sales, turnover or gross receipt exceeds ten lakh rupees.

II. Newly set up business, income exceeds One lakh twenty thousand or total sales, turnover or gross receipt exceeds ten lakh rupees.

(Rest other conditions are common for all)

C. If the assessee has claimed income under section 44AE, 44BB or 44BBB and he claim his income below the limit define under the section.

D. If the assessee follows section 44AE & his to total income exceeds invoice chargeable to tax.

The books of accounts which specific professional need to maintain :

1. Cash book

2. Journal

3. Ledger

4. Carbon copies of Bill

Medical professional need to maintain additional records :

(1) Daily cash register as per Form no. 3C

(2) Inventory record

Period - The books and records are to be maintain for six assessment year and to be maintained at the principle place of business.